SS Innovations and the Rise of Indian Surgical Robotics

SS Innovations ran the world's longest-distance telesurgery, Guyana to Indore, on a system priced at a tenth of da Vinci. Behind the headline is a recurring-services medtech scaling fast, with cash-burn the catch.

Manik Gupta

Founder and editor of DeepTech India. Manik writes about India's frontier technology ecosystem — AI, semiconductors, space, quantum, robotics and biotech — translating research and policy into clear, reliable reporting.

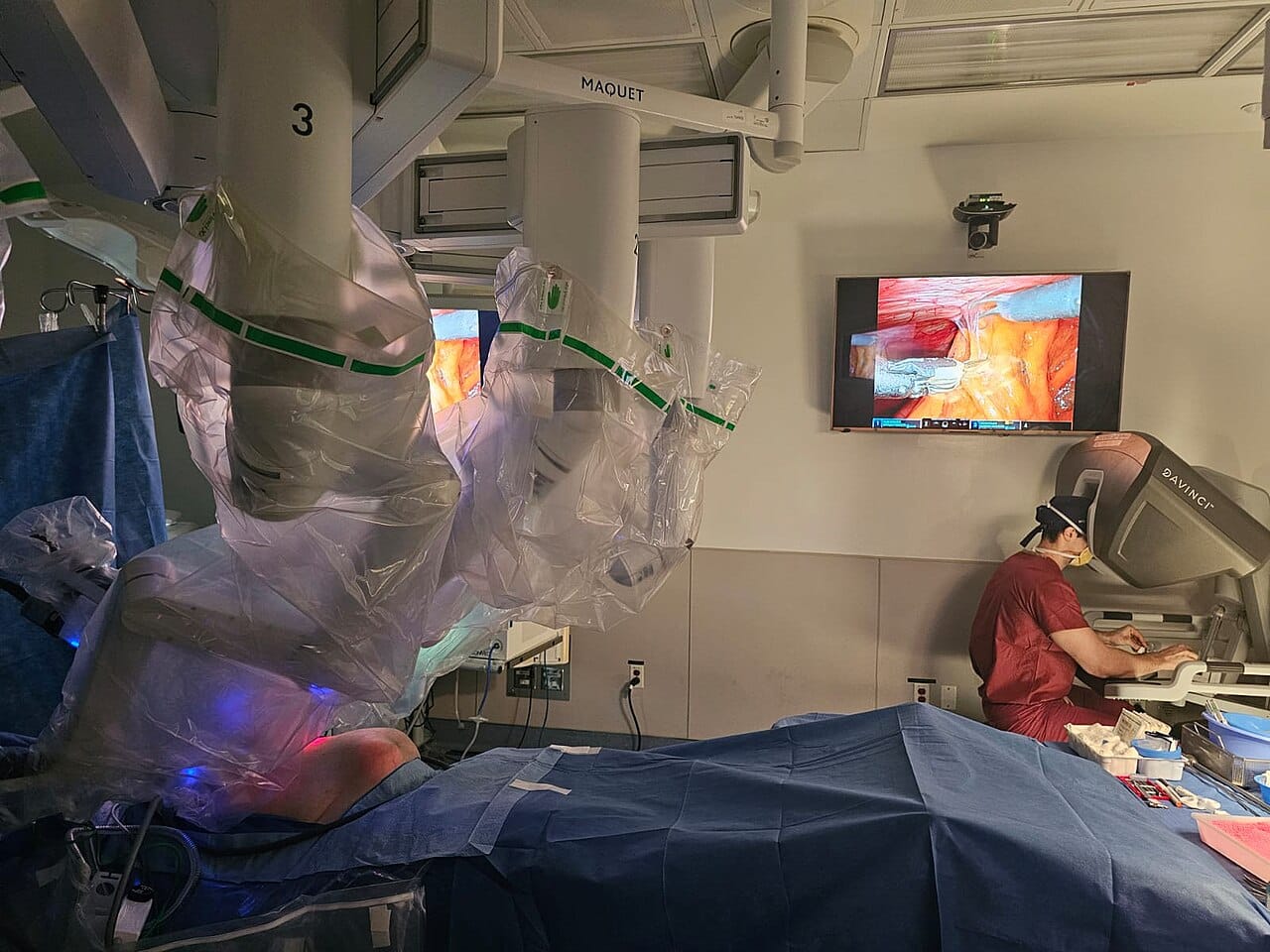

On 4 June 2026, a surgeon in Guyana operated on a robotic surgical platform sitting roughly 20,000 kilometres away in Indore, India. Dr. Sudhir Srivastava, founder and chairman of SS Innovations International (Nasdaq: SSII), drove the procedure from a MantrAsana tele-surgeon console, with commands traversing intercontinental network links at a round-trip latency the company puts at 290 to 300 milliseconds. SS Innovations calls it the world's longest-distance robotic telesurgery. The clinical and engineering claim matters less than what it signals: an Indian company is now defining the operating envelope for remote surgery, a category its much larger US incumbent does not address at all.

The milestone is one data point in a steep commercialisation curve. SS Innovations reports 173 telesurgeries to date, of which 22 were cardiac, and more than 10,500 cumulative surgeries on its SSi Mantra system. For an asset class that institutional investors have historically equated with a single name, Intuitive Surgical, the arrival of a credible, cheaper, telesurgery-capable challenger out of India reframes the competitive map.

The latency problem, and why distance is the hard part

Remote surgery is fundamentally a control-loop problem. The surgeon's hand motions at the console must be digitised, transmitted, executed by the patient-side arms, and the resulting endoscopic video returned, all fast enough that the operator perceives the instruments as an extension of their hands. Above roughly 300 milliseconds of round-trip delay, most surgeons begin to compensate by moving more slowly and deliberately, and the risk of overshoot rises. The 290-to-300 ms figure SS Innovations reports for a Guyana-to-Indore link is therefore close to the practical ceiling, and clearing a transcontinental procedure at that latency is a non-trivial systems-engineering result.

Achieving it requires more than a fast pipe. It demands deterministic, low-jitter networking, aggressive but lossless video compression, predictive motion handling, and fail-safe logic that freezes the instruments if the link degrades. The MantrAsana console and the SSi Mantra patient cart are the visible hardware; the defensible work sits in the real-time software stack that keeps a 20,000-km loop stable. That capability is what converts a single hospital sale into a network: one tertiary centre can, in principle, supervise or perform procedures across multiple under-served sites.

It is worth stating the obvious caveat. These are company-reported figures on a small base of 173 telesurgeries, not peer-reviewed multi-centre outcomes, and "longest distance" is a record that invites contest. Telesurgery at scale also depends on regulatory acceptance, clinical liability frameworks, and network guarantees that do not yet exist in most jurisdictions. The capability is real; the addressable clinical practice around it is still nascent.

The unit economics: a 10x cost wedge

The investment thesis rests less on the telesurgery headline than on price. SS Innovations positions the SSi Mantra at roughly one-tenth the cost of Intuitive's da Vinci. That gap is the moat. A da Vinci system and its consumables price robotic surgery out of reach for most hospitals outside high-income markets; a platform at a tenth of the capital cost expands the serviceable market to Tier-2 and Tier-3 hospitals across India, Africa, Southeast Asia and Latin America that could never amortise a Western system.

Crucially, da Vinci is not cleared for telesurgery. SS Innovations is competing in an adjacent envelope the incumbent does not occupy, while undercutting it on the core robotic-surgery proposition. That is a rare position: cheaper on the overlapping product and differentiated on a capability the leader lacks.

The financials show the wedge converting into revenue. For Q1 2026, reported in May, SS Innovations posted revenue of $11.1 million, up 116.8% year on year, at a 48% gross margin, with 26 system installations in the quarter. The model is the familiar razor-and-blade structure of surgical robotics: an upfront system sale followed by recurring instrument, accessory and service revenue per procedure. As the installed base compounds past 10,500 cumulative surgeries, the recurring services layer should become the durable part of the P&L. A 48% gross margin is respectable for a hardware-led medtech still scaling manufacturing, though well below the 65%-plus margins Intuitive enjoys at maturity, which is the bull-case operating-leverage story if volumes hold.

Regulatory footprint and the US prize

Geographic expansion is the second pillar. SS Innovations has secured regulatory clearances and entered markets including Sri Lanka, Kenya and Indonesia, precisely the cost-sensitive, infrastructure-constrained settings where a tenth-the-price system has the strongest pull and where telesurgery could extend specialist reach into regions with few trained robotic surgeons.

The larger catalyst is the United States. The company is pursuing an FDA De Novo classification for the SSi Mantra 3. De Novo is the pathway for novel devices that lack a clear predicate but pose low-to-moderate risk, and it is slower and less certain than the 510(k) route. Clearance would open the world's largest surgical-robotics market and validate the platform against the most demanding regulator, but the timeline is open-ended and approval is not assured. Investors should treat the US as optionality, not a base case.

Risks: cash burn and dilution

The honest risk in this story is the balance sheet. Scaling a hardware medtech, funding a US regulatory campaign, building international service infrastructure and sustaining R&D is capital-intensive, and a company growing revenue triple digits off a roughly $11 million quarterly base is not self-funding that build. Continued cash burn and the prospect of equity dilution are the central watch-items. As a Nasdaq-listed name, SS Innovations can tap public markets, but dilution at a depressed multiple is the recurring hazard for pre-scale medtech, and a slip in the FDA timeline or a slowdown in system installs would pressure the financing runway directly.

There is also concentration and execution risk. The narrative leans heavily on the founder, Dr. Srivastava, and on continued clinical wins; the telesurgery results, while striking, rest on small numbers. Competitive response from Intuitive and from other emerging-market entrants, plus the long, uneven path to telesurgery reimbursement and liability frameworks, all temper the timeline.

The forward view

What SS Innovations is building is less a product than a category bridge: affordable robotic surgery for the markets the incumbents priced out, with a telesurgery capability that turns specialist scarcity from a constraint into an addressable opportunity. If the 48% gross margin holds and the recurring-services base compounds as installs climb, the unit economics improve structurally with scale. The Guyana-to-Indore procedure is best read not as a stunt but as a proof that the control stack works at the edge of the latency envelope, and that an Indian medtech now sets the frontier in a field long defined by a single American name. The next two proof points to watch are the FDA De Novo decision and whether the company can fund its expansion without diluting shareholders into the growth.

Tags

More from Robotics

VECROS Unveils Jetcore, an India-Designed 'Brain' for Drones That Fly Without GPS

Bengaluru-based deep-tech startup VECROS has unveiled Jetcore, an India-designed AI autonomy compute platform that lets drones and robots localise, map and navigate on their own in GPS-denied environments — packaging the "brain" of its ATHERA drone for other manufacturers to build around.

Yaanendriya Raises ₹15 Crore to Build India's Own Navigation and Inertial Sensors

Bengaluru deep-tech startup Yaanendriya has raised ₹15 crore in a seed round led by Piper Serica to scale its indigenous inertial sensors and navigation controllers for drones, robots, space and defence — including an MoU to supply the Indian Army's 515 Army Base Workshop.